Navigating Risk: Your Guide to Contractor Insurance and Bonds

Introduction: Why Every Contractor Needs a Risk Plan

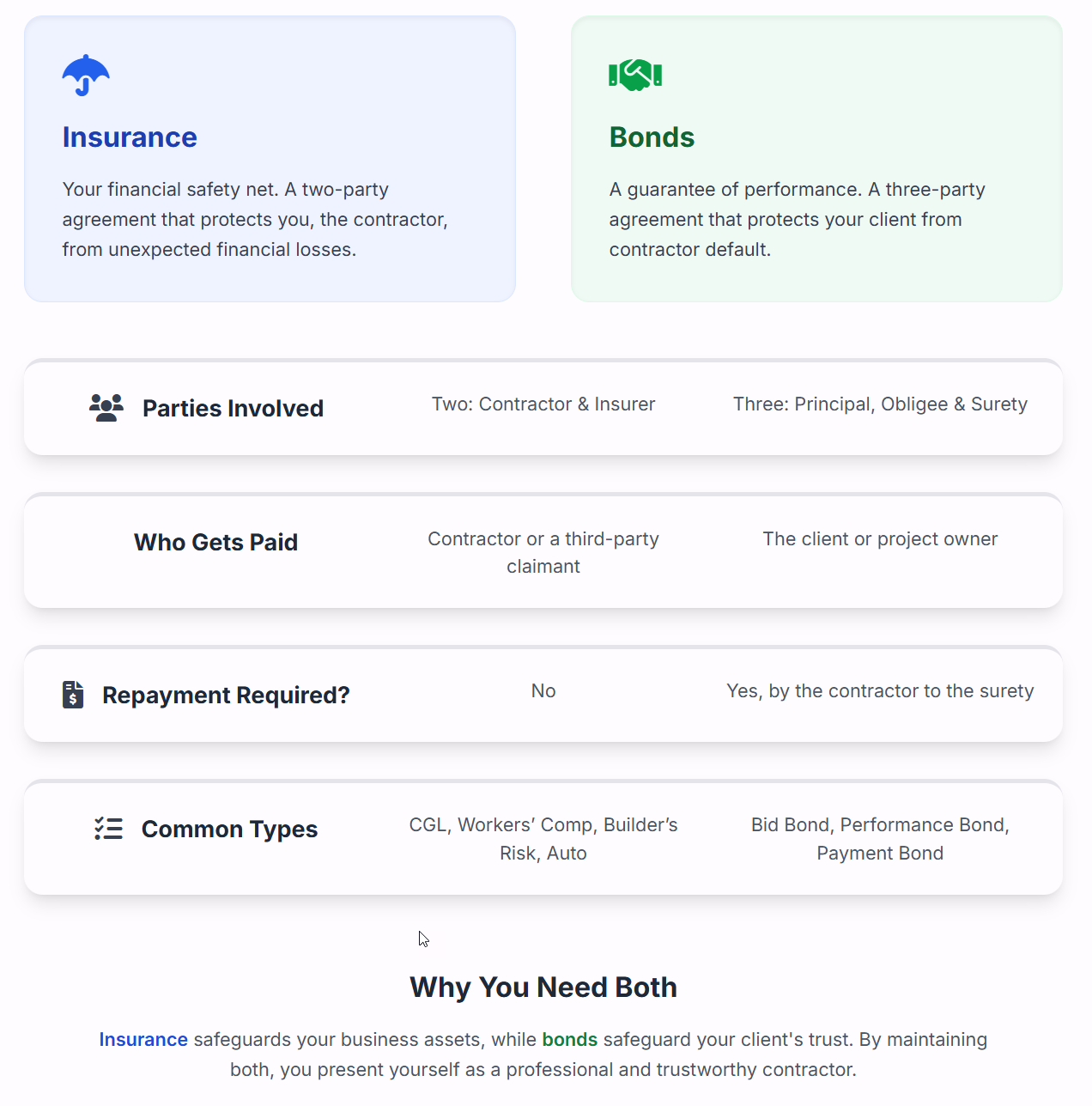

In the construction world, risk is inevitable. From a workplace injury to an unexpected project delay, a single incident can derail your schedule and drain your finances. That’s why every contractor needs a clear strategy for risk management — and that strategy starts with understanding insurance and bonds.

While both serve as safeguards, they have very different purposes. In simple terms:

Insurance protects you.

Bonds protect your client.

Insurance: Your Safety Net

Insurance is like your financial safety harness — it’s a two-party agreement between you and an insurance carrier, designed to protect you from unexpected losses.

Key Insurance Coverages for Contractors

Commercial General Liability (CGL) – Protects against claims of bodily injury, property damage, and personal injury caused by your operations or occurring on your premises.

Workers’ Compensation – Required for Florida construction employers with one or more employees. Covers medical costs and lost wages for jobsite injuries.

Builder’s Risk Insurance – Covers buildings and materials while a project is under construction.

Business Automobile Insurance – Protects against accidents involving company vehicles.

💡 Pro Tip: Even if you’re self-employed, certain clients may require proof of specific coverage before signing a contract.

Bonds: A Guarantee of Performance

A surety bond is not insurance — it’s a three-party agreement that guarantees you’ll fulfill your contractual obligations.

The Three Parties in a Surety Bond:

Principal – You, the contractor, promising to complete the work.

Obligee – The project owner or client receiving the guarantee.

Surety – The bond company backing your promise financially.

If you fail to perform, the Surety compensates the Obligee — but you must repay the Surety for any amount they cover.

What Sureties Look For: The Three C’s

When evaluating your bond application, surety companies assess:

Character – Your reputation, integrity, and track record.

Capacity – Your ability and resources to complete the work.

Capital – Your financial stability and liquidity.

Insurance vs. Bonds: Quick Comparison Table

By maintaining both, you position yourself as a professional, trustworthy contractor — one who’s prepared for the unexpected and committed to delivering results.

Final Word

In construction, risk isn’t optional — but being unprepared is. Understanding the difference between insurance and bonds is the first step toward building a secure, thriving contracting business in Florida.

Generated Article by LLA Founder Kevin Baird